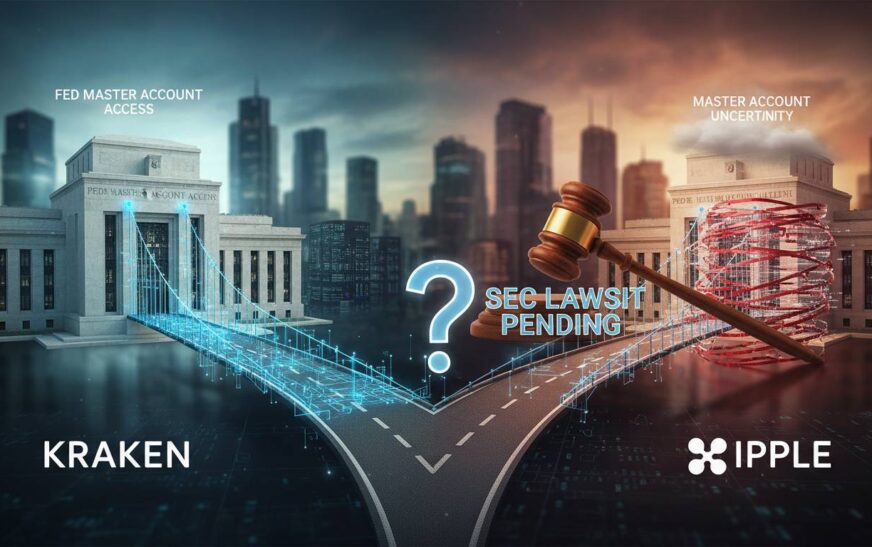

Kraken Financial, the Wyoming-chartered banking arm of the cryptocurrency exchange Kraken, has achieved a historic milestone by securing a limited-purpose Federal Reserve master account. This development raises a compelling question: could Ripple, another major crypto player, follow suit with its own master account?

Historic Milestone: Kraken Gains Fed Access

On March 4, 2026, Kraken Financial became the first digital-asset-focused institution in U.S. history to receive a Federal Reserve master account, granted by the Federal Reserve Bank of Kansas City . This limited-purpose account allows direct access to Fedwire, enabling Kraken to settle U.S. dollar transactions without relying on intermediary banks .

The approval follows more than five years of regulatory engagement, operational scrutiny, and coordination with Wyoming and federal regulators . While Kraken gains direct connectivity to core payment rails, it does not receive full banking privileges—such as earning interest on reserves or accessing the discount window .

Significance of the Master Account Access

Faster, More Efficient Transactions

With direct Fedwire access, Kraken can now process institutional client transactions more quickly and efficiently, reducing costs and operational complexity .

Regulatory Validation

This approval signals growing regulatory acceptance of crypto infrastructure as part of the broader financial system. Arjun Sethi, Co‑CEO of Payward (Kraken’s parent company), described the moment as the convergence of crypto infrastructure with sovereign financial rails .

Industry Pushback

Traditional banking groups, including the Bank Policy Institute and The Clearing House Association, expressed concern over the lack of transparency and potential risks to financial stability posed by granting crypto firms direct access to Fed systems .

Could Ripple Follow with Its Own Master Account?

Ripple’s Regulatory Moves

In July 2025, Ripple applied for a national banking charter from the Office of the Comptroller of the Currency (OCC) and submitted a request for a Federal Reserve master account via Standard Custody, a trust company it acquired . The move aimed to enhance trust in its RLUSD stablecoin by aligning reserves and settlement closer to the Fed’s infrastructure .

Legal and Structural Hurdles

Caitlin Long, CEO of Custodia Bank, emphasized that trust companies—including Ripple’s Standard Custody—are not legally eligible for Fed master accounts unless they become true depository institutions. Trust charters, she argues, cannot accept U.S. dollar deposits or access Fedwire/ACH .

The Federal Reserve’s Account Access Guidelines reinforce this distinction, subjecting non-depository institutions to the most stringent review and often denying access even when eligibility is claimed .

Regulatory Precedents and Developments

In December 2025, the OCC granted conditional approval for Ripple to establish a national trust bank charter—though this does not equate to a depository institution or guarantee Fed access .

Meanwhile, Fed Governor Christopher Waller has proposed a “payment account” model—a lighter, payments-only version of a master account—for fintech and crypto innovators . This framework could potentially open the door for firms like Ripple, but it remains in prototype stage.

Analysis: Ripple’s Path Forward

Structural Transformation Required

For Ripple to gain Fed master account access, it would likely need to convert its trust charter into a full depository institution, meeting capital, governance, and risk-management standards required for bank status .

Regulatory Momentum and Innovation

The Fed’s approval of Kraken under a “skinny” or limited-purpose framework may serve as a pilot for broader inclusion of crypto firms. If successful, this model could be extended to other qualified institutions, potentially including Ripple—if it meets eligibility criteria .

Market and Policy Implications

Ripple’s access to a Fed master account would enhance settlement efficiency for its stablecoin products and strengthen institutional trust. However, it would also intensify scrutiny from regulators and banking incumbents concerned about systemic risk and regulatory parity.

Conclusion

Kraken’s historic approval for a limited-purpose Federal Reserve master account marks a turning point in crypto’s integration with traditional finance. While Ripple has taken steps toward similar access, significant legal and structural barriers remain. Trust charters are not sufficient—only depository institutions qualify for Fed master accounts under current regulations. That said, emerging frameworks like the Fed’s proposed “payment account” could offer a pathway forward if Ripple adapts its structure and regulatory posture.

As the crypto industry evolves, the question of whether Ripple can follow Kraken’s lead remains open—but increasingly plausible, provided it navigates the complex regulatory landscape.

Frequently Asked Questions

What exactly did Kraken gain with its Fed master account?

Kraken Financial received a limited-purpose master account from the Federal Reserve Bank of Kansas City on March 4, 2026. This grants direct access to Fedwire for faster, more efficient settlement, but excludes full banking privileges like interest on reserves or access to the discount window .

Why can’t trust companies like Ripple’s Standard Custody get Fed access?

Trust charters are legally prohibited from accepting U.S. dollar deposits and accessing Fedwire or ACH. The Fed’s guidelines require institutions to be depository institutions to qualify for master accounts .

Has Ripple taken steps toward eligibility?

Yes. In July 2025, Ripple applied for a national trust bank charter and a Fed master account via Standard Custody. In December 2025, the OCC granted conditional approval for Ripple to establish a national trust bank, though this does not yet qualify it as a depository institution .

What is the Fed’s “payment account” proposal?

Fed Governor Christopher Waller has proposed a lighter, payments-only account model for fintech and crypto firms. This “payment account” would offer limited access to Fed payment rails without full master account privileges, but it remains in prototype stage .

Could Ripple realistically gain Fed access soon?

Only if Ripple transitions from a trust charter to a depository institution and meets regulatory standards. The Fed’s evolving framework may eventually accommodate such firms, but significant legal and structural changes are required.

What does Kraken’s approval mean for the crypto industry?

Kraken’s access signals growing regulatory acceptance of crypto infrastructure. It may pave the way for other regulated crypto firms to gain similar access, provided they meet eligibility and risk standards .

The post Kraken Gains Fed Access: Could Ripple Follow With Its Own Master Account? appeared first on Crunchtime News.